A technique succeeds in mathematical physics, not by a clever trick, or a happy accident, but because it expresses some aspect of physical truth (O. G. Sutton)

Imagine three unbalanced coins:

- Coin 1: Probability of head=0.495 and probability of tail=0.505

- Coin 2: Probability of head=0.745 and probability of tail=0.255

- Coin 3: Probability of head=0.095 and probability of tail=0.905

Now let’s define two games using these coins:

- Game A: You toss coin 1 and if it comes up head you receive 1€ but if not, you lose 1€

- Game B: If your present capital is a multiple of 3, you toss coin 2. If not, you toss coin 3. In both cases, you receive 1€ if coin comes up head and lose 1€ if not.

Played separately, both games are quite unfavorable. Now let’s define Game A+B in which you toss a balanced coin and if it comes up head, you play Game A and play Game B otherwise. In other words, in Game A+B you decide between playing Game A or Game B randomly.

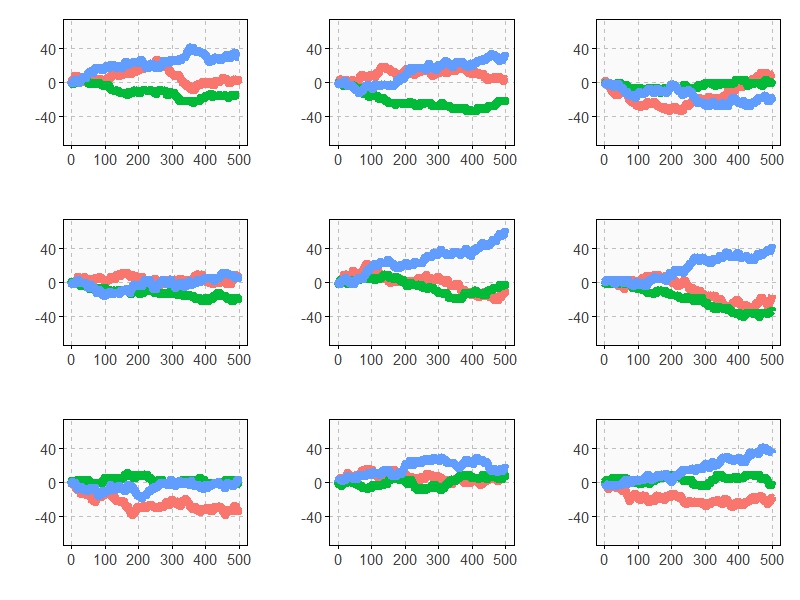

Starting with 0€, it is easy to simulate the three games along 500 plays. This is an example of one of these simulations:

Resulting profit of Game A+B after 500 plays is +52€ and is -9€ and -3€ for Games A and B respectively. Let’s do some more simulations (I removed legends and titles but colors of games are the same):

As you can see, Game A+B is the most profitable in almost all the previous simulations. Coincidence? Not at all. This is a consequence of the stunning Parrondo’s Paradox which states that two losing games can combine into a winning one.

If you still don’t believe in this brain-crashing paradox, following you can see the empirical distributions of final profits of three games after 1.000 plays:

After 1000 plays, mean profit of Game A is -13€, is -7€ for Game B and 17€ for Game A+B.

This paradox was discovered in the last nineties by the Spanish physicist Juan Parrondo and can help to explain, among other things, why investing in losing shares can result in obtaining big profits. Amazing:

require(ggplot2)

require(scales)

library(gridExtra)

opts=theme(

legend.position = "bottom",

legend.background = element_rect(colour = "black"),

panel.background = element_rect(fill="gray98"),

panel.border = element_rect(colour="black", fill=NA),

axis.line = element_line(size = 0.5, colour = "black"),

axis.ticks = element_line(colour="black"),

panel.grid.major = element_line(colour="gray75", linetype = 2),

panel.grid.minor = element_blank(),

axis.text.y = element_text(colour="gray25", size=15),

axis.text.x = element_text(colour="gray25", size=15),

text = element_text(size=20),

plot.title = element_text(size = 35))

PlayGameA = function(profit, x, c) {if (runif(1) < c-x) profit+1 else profit-1}

PlayGameB = function(profit, x1, c1, x2, c2) {if (profit%%3>0) PlayGameA(profit, x=x1, c=c1) else PlayGameA(profit, x=x2, c=c2)}

####################################################################

#EVOLUTION

####################################################################

noplays=500

alpha=0.005

profit0=0

results=data.frame(Play=0, ProfitA=profit0, ProfitB=profit0, ProfitAB=profit0)

for (i in 1:noplays) {results=rbind(results, c(i,

PlayGameA(profit=results[results$Play==(i-1),2], x =alpha, c =0.5),

PlayGameB(profit=results[results$Play==(i-1),3], x1=alpha, c1=0.75, x2=alpha, c2=0.1),

if (runif(1)<0.5) PlayGameA(profit=results[results$Play==(i-1),4], x =alpha, c =0.5) else PlayGameB(profit=results[results$Play==(i-1),4], x1=alpha, c1=0.75, x2=alpha, c2=0.1)

))}

results=rbind(data.frame(Play=results$Play, Game="A", Profit=results$ProfitA),

data.frame(Play=results$Play, Game="B", Profit=results$ProfitB),

data.frame(Play=results$Play, Game="A+B", Profit=results$ProfitAB))

ggplot(results, aes(Profit, x=Play, y=Profit, color = Game)) +

scale_x_continuous(limits=c(0,noplays), "Plays")+

scale_y_continuous(limits=c(-75,75), expand = c(0, 0), "Profit")+

labs(title="Evolution of profit games along 500 plays")+

geom_line(size=3)+opts

####################################################################

#DISTRIBUTION

####################################################################

noplays=1000

alpha=0.005

profit0=0

results2=data.frame(Play=numeric(0), ProfitA=numeric(0), ProfitB=numeric(0), ProfitAB=numeric(0))

for (j in 1:100) {results=data.frame(Play=0, ProfitA=profit0, ProfitB=profit0, ProfitAB=profit0)

for (i in 1:noplays) {results=rbind(results, c(i,

PlayGameA(profit=results[results$Play==(i-1),2], x =alpha, c =0.5),

PlayGameB(profit=results[results$Play==(i-1),3], x1=alpha, c1=0.75, x2=alpha, c2=0.1),

if (runif(1)<0.5) PlayGameA(profit=results[results$Play==(i-1),4], x =alpha, c =0.5)

else PlayGameB(profit=results[results$Play==(i-1),4], x1=alpha, c1=0.75, x2=alpha, c2=0.1)))}

results2=rbind(results2, results[results$Play==noplays, ])}

results2=rbind(data.frame(Game="A", Profit=results2$ProfitA),

data.frame(Game="B", Profit=results2$ProfitB),

data.frame(Game="A+B", Profit=results2$ProfitAB))

ggplot(results2, aes(Profit, fill = Game)) +

scale_x_continuous(limits=c(-150,150), "Profit")+

scale_y_continuous(limits=c(0,0.02), expand = c(0, 0), "Density", labels = percent)+

labs(title=paste("Parrondo's Paradox (",as.character(noplays)," plays)",sep=""))+

geom_density(alpha=.75)+opts